European stocks slip as US-Iran talks stall over excessive demands

European equity markets turned lower on Monday after US-Iran negotiations hit a snag, with both sides accusing each other of making excessive demands.

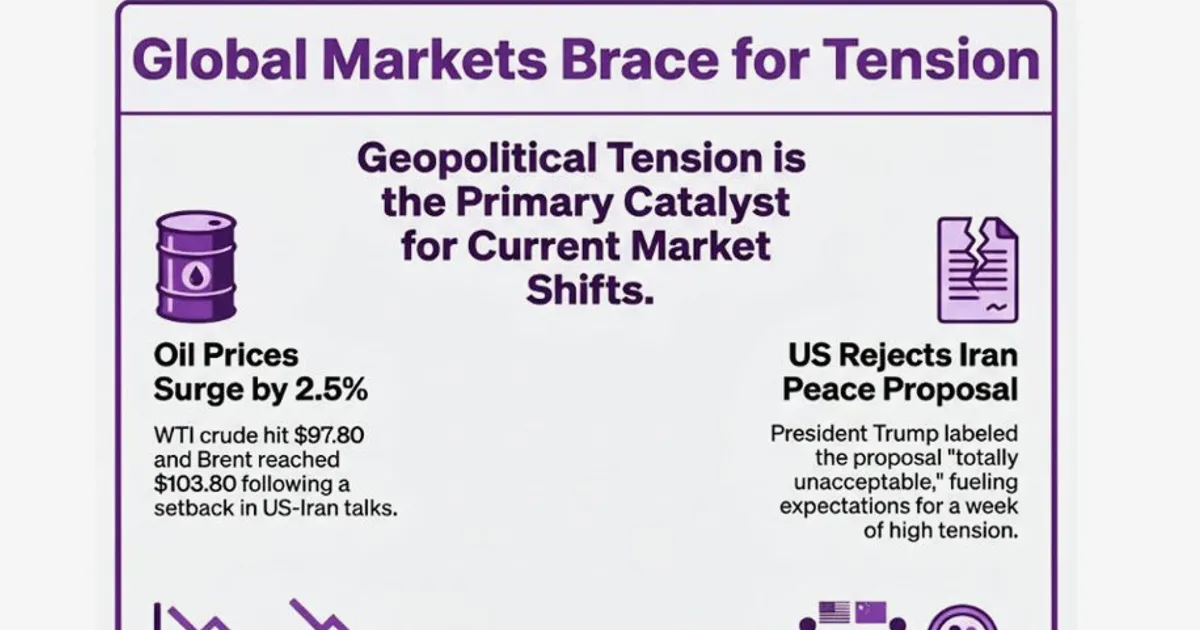

European equity markets slipped into negative territory on Monday as optimism over a potential US-Iran deal faded over the weekend. Both sides accused each other of making unreasonable demands, with President Trump calling Iran's proposal "totally unacceptable." The breakdown in talks removes a key source of geopolitical risk premium that had been compressing in recent sessions. For interest rate traders, this means renewed uncertainty that could support safe-haven flows into government bonds, potentially weighing on yields. The shift in sentiment is visible in real-time price charts on NowPrice, where European bond futures have edged higher alongside the dip in equities.

This geopolitical risk resurgence complicates the outlook for central banks, particularly the Federal Reserve, which operates under a dual mandate of maximum employment and price stability. While the Fed has been focused on inflation, a flight to safety could steepen the yield curve if long-term bonds rally more than short-term ones, potentially reversing recent flattening. The term premium—the compensation investors demand for holding longer-dated debt—may rise as uncertainty increases, affecting the decomposition of yields. Meanwhile, the European Central Bank's Transmission Protection Instrument (TPI) could be tested if risk-off sentiment spreads to peripheral sovereign bonds, though the ECB has tools to prevent unwarranted fragmentation. The US-Iran impasse also keeps energy prices elevated, adding to inflationary pressures that complicate monetary policy decisions. Swap spreads, which reflect counterparty risk and liquidity, may widen as market participants reassess the probability of a negotiated settlement.

Looking ahead, market attention is likely to pivot toward US-China relations as Trump prepares to visit Beijing later this week. Any fresh trade tensions could further amplify risk-off positioning, while the US-Iran impasse keeps energy prices elevated. Traders will watch for any official statements from either side that might signal a path back to the negotiating table. Additionally, the Fed's balance sheet runoff continues, and any sudden shift in risk appetite could alter the pace of quantitative tightening, as seen during previous geopolitical shocks. Yield-curve inversion dynamics will be closely monitored, as a deeper inversion could signal recession fears, while a steepening might indicate expectations of future rate cuts. The interplay between geopolitical developments and central bank responses will be key for fixed-income markets in the coming sessions.