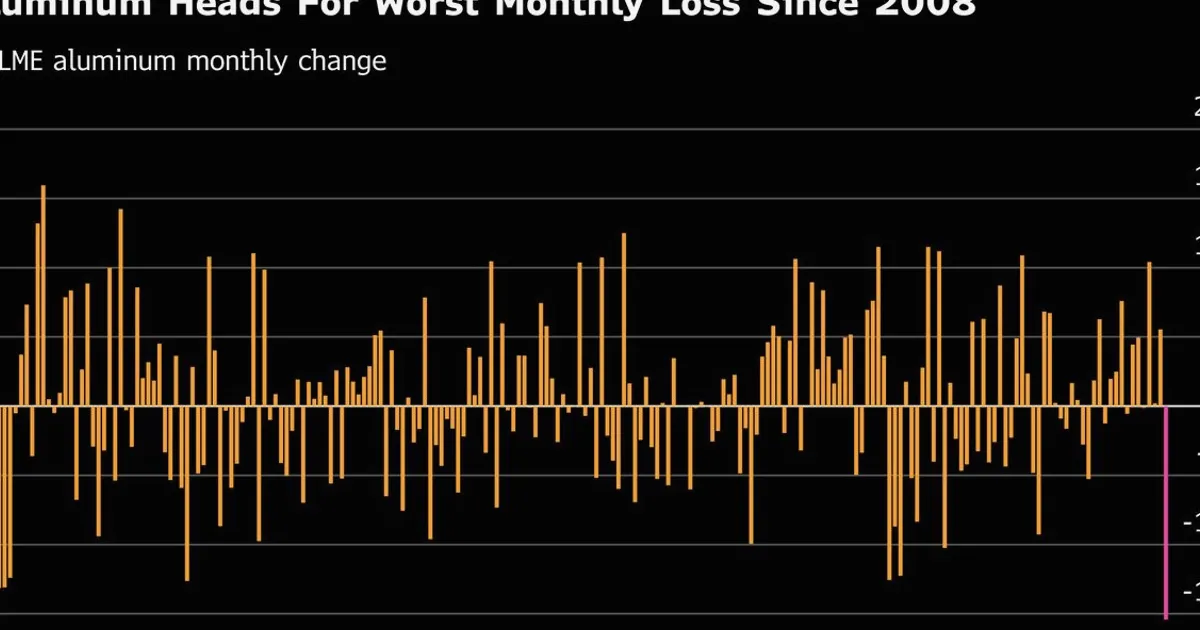

Aluminum Heads for Worst Monthly Drop Since 2008 on Supply Rebound

Aluminum prices are on track for their steepest monthly decline since 2008 as expectations of restored Middle Eastern supply unwind the war-driven rally.

Aluminum prices are on track for their steepest monthly decline since 2008, driven by expectations that lost Middle Eastern supply will soon return to the market. The metal has rapidly unwound the rally triggered by geopolitical tensions earlier this year, as traders price in a normalization of output from key producing regions. London Metal Exchange three-month aluminum futures have fallen over 15% in February, heading for the worst monthly performance since the global financial crisis. The sell-off accelerated after reports that major smelters in the Gulf region are restarting operations following a temporary shutdown due to regional instability. This supply recovery is overwhelming demand concerns, with inventories in LME-registered warehouses rising for the first time in months.

For commodities traders, this sharp reversal highlights how quickly supply-driven premiums can evaporate when the perceived risk subsides. The aluminum market had priced in a significant disruption premium following the Iran conflict, but as diplomatic channels reopen and production resumes, that premium is being aggressively stripped out. The mechanism is straightforward: when supply threats materialize, prices spike as buyers scramble for available metal; when those threats fade, the same buyers unwind positions, causing a rapid price decline. This pattern is common in commodity markets, where geopolitical risk is often transient. Traders monitoring the NowPrice commodities page can track real-time aluminum prices and compare them to other base metals like copper and zinc to gauge relative strength across the complex.

Looking ahead, the key focus will be on actual production data from Middle Eastern smelters and any official statements regarding output restoration. Specifically, traders will watch for weekly production figures from the Gulf region and any announcements from state-owned producers about capacity utilization rates. Additionally, global demand signals from China, the world's largest aluminum consumer, and the manufacturing sector will determine whether the current sell-off extends or finds a floor. Chinese economic data, including industrial production and PMI readings, will be critical. Traders should also watch for any unexpected supply disruptions, such as power outages or labor strikes, that could reignite volatility. The aluminum market remains sensitive to both supply and demand shocks, and the current downtrend could reverse quickly if new disruptions emerge.