India Bond Yields Under Pressure From Rate Hike Bets and Fiscal Worries

Indian bond yields face further upside risk as markets price in potential rate hikes and deteriorating fiscal outlook, adding to pressure on the Reserve Bank of India's policy stance.

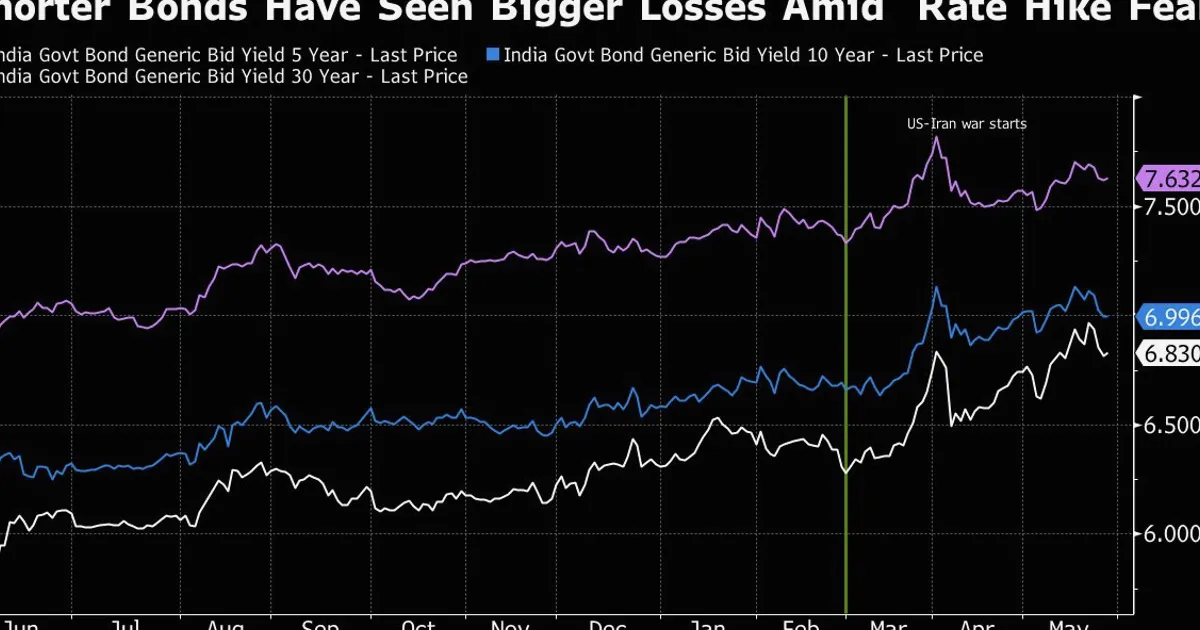

Indian bond yields have surged recently and may extend their rise as investors weigh the prospects of interest-rate hikes amid growing concerns over the government's fiscal position. The pressure on yields reflects a combination of domestic inflation risks and global monetary tightening expectations, which are testing the Reserve Bank of India's (RBI) policy credibility.

The recent move in yields matters for interest rate traders because it signals a repricing of the RBI's policy path. If the government's fiscal deficit widens beyond targets, the RBI may be forced to hike rates to contain inflation, which would further push yields higher. This dynamic is reminiscent of the taper tantrum episodes when fiscal dominance concerns led to sharp bond selloffs. For traders, the widening spread between Indian and US yields could attract foreign capital, but only if the RBI maintains a hawkish stance. Check NowPrice's rates page for the latest Indian government bond yields and policy rate expectations.

Looking ahead, traders should watch the upcoming Union Budget for fiscal consolidation signals, as well as RBI's monetary policy meetings. Any deviation from the fiscal deficit target could trigger another leg higher in yields. Additionally, global factors such as US Federal Reserve rate decisions and crude oil prices will influence India's inflation outlook and, consequently, bond market dynamics. The key level to monitor is the 10-year yield's reaction around the 7.5% mark, which has acted as resistance in recent sessions.