India Money Market Volumes Hit Record on Bank Lending Boom

India's money-market turnover surged to a record high as state-owned banks ramped up borrowing to meet booming credit demand, signaling strong economic activity and potential liquidity tightening.

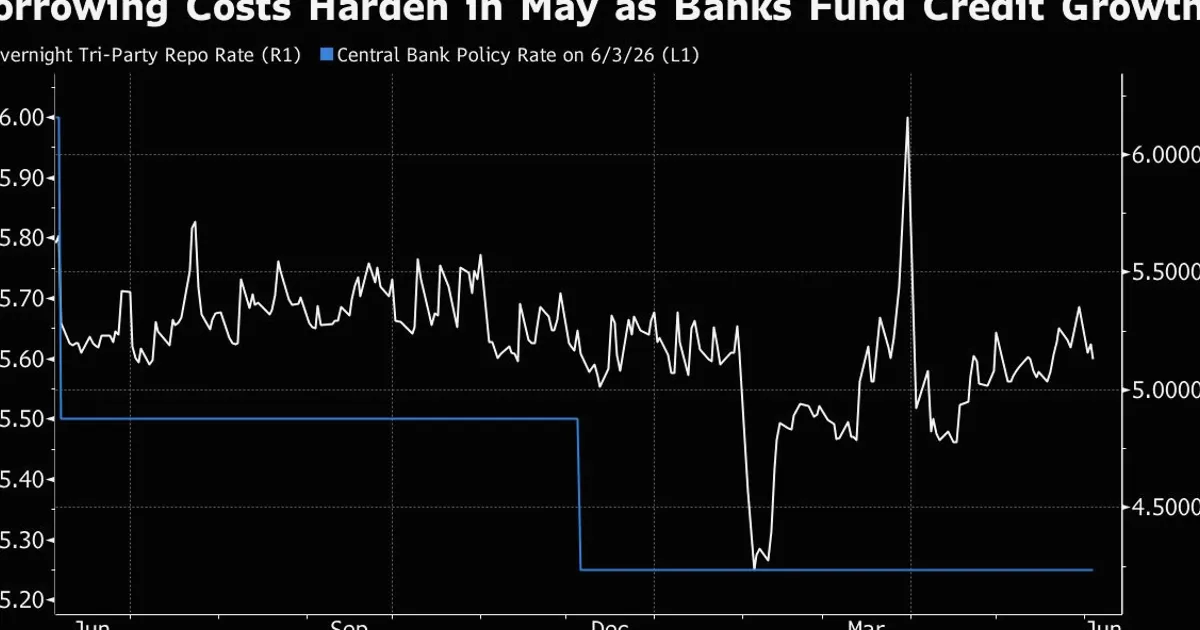

India's money-market turnover jumped to a record high as state-owned lenders stepped up borrowing to fund booming credit demand, according to Bloomberg data. The surge reflects a sharp increase in short-term funding needs amid robust economic growth and rising loan disbursements. This development is closely tied to the broader financial landscape, where the earnings yield on Indian equities (the inverse of the forward P/E ratio) currently hovers around 5.5%, compared to the 10-year government bond yield near 7%. The resulting negative gap under the so-called Fed model suggests stocks are relatively expensive versus bonds, a dynamic that can influence capital flows. Meanwhile, the Nifty 50's forward P/E of ~20x sits above its 5-year average of 18.5x, indicating elevated valuations that may be supported by strong earnings growth but also vulnerable to rate shocks.

For stock market participants, the record money-market volumes signal strong credit demand, which typically supports corporate earnings and economic expansion. However, the increased borrowing by state banks could also tighten liquidity in the banking system, potentially pushing up short-term interest rates. Higher rates may pressure interest-sensitive sectors like real estate and consumer finance, while benefiting banks with wider net interest margins. Traders can monitor these dynamics on NowPrice's live stocks dashboard to track sector rotation and rate-sensitive stocks. Notably, breadth indicators such as the advance-decline line have weakened in recent weeks, suggesting that the rally is narrowing. Sector rotation has favored financials and IT, while consumer discretionary and real estate have lagged. Buyback yields, which averaged 1.2% across the Nifty 50 last year, could provide a floor for stocks if rates rise further, as companies may opt to return cash to shareholders rather than invest in capex.

Looking ahead, investors should watch the Reserve Bank of India's liquidity management operations and any signals on policy rates. The sustainability of credit growth and its impact on inflation will be key. Data on industrial production and loan growth in the coming weeks will provide further clues on the trajectory of the economy and monetary policy. Additionally, options-implied volatility on the Nifty 50 has risen to 14.5%, above its 3-month average of 12%, indicating heightened uncertainty around rate decisions. A sustained rise in short-term rates could compress forward P/E multiples, particularly for high-growth sectors. Conversely, if credit growth moderates without derailing earnings, the current valuation premium may persist. Investors should also monitor the RBI's open market operations and any changes in the cash reserve ratio, as these tools directly impact liquidity and short-term rates.