Wheat Extends Decline as Traders Digest Iran Ceasefire Talks

Wheat futures are extending their longest losing streak since January as traders assess the potential for a ceasefire in the Middle East, which could ease supply concerns and weigh on prices.

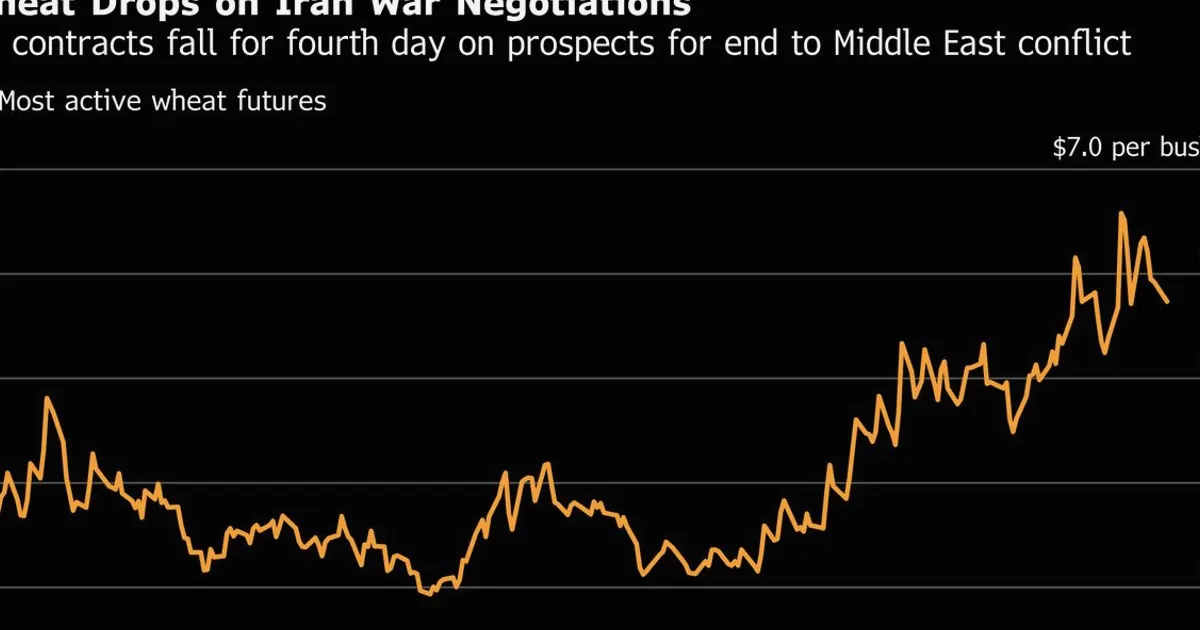

Wheat futures are extending their longest losing streak since January, as traders returning from a US holiday digest progress in negotiations to end the war in the Middle East. The decline reflects growing expectations that a ceasefire could reduce geopolitical risk premiums embedded in grain markets. Wheat for delivery in May fell 1.2% to $5.45 per bushel on the Chicago Board of Trade, marking the fifth consecutive session of losses. The streak is the longest since a six-day decline in late January, according to data compiled by Bloomberg.

For commodities traders, the key dynamic is the potential easing of supply disruptions. The Middle East conflict has historically affected wheat prices through shipping route disruptions and uncertainty over Black Sea exports. A ceasefire would likely remove a significant risk premium, pushing prices lower. The risk premium is the extra cost that traders build into futures prices to account for the possibility of supply shocks, such as the closure of key shipping lanes like the Strait of Hormuz or disruptions to grain shipments from Ukraine and Russia. Without these risks, prices could fall toward levels more closely aligned with underlying supply and demand fundamentals. Live commodities prices and charts on NowPrice show how the market is reacting to each development in real time, offering traders a tool to track volatility as negotiations unfold.

Looking ahead, traders will monitor official statements from Iran and other parties, as well as any concrete ceasefire agreements. Additionally, attention remains on global wheat supply fundamentals, including harvest progress in the Northern Hemisphere and export policies from major producers like Russia and Ukraine. The next major data point is the USDA's weekly export sales report, which will provide further clues on demand trends. Analysts expect the report to show export sales of 300,000 to 600,000 metric tons for the 2024/25 marketing year, compared with 450,000 tons in the previous week. A weaker-than-expected reading could add further downward pressure on prices, while strong demand may help stabilize the market.