UK mortgage approvals rise in April, stay above six-month average

UK mortgage approvals rose to 65,900 in April, above the six-month average of 63,100, signaling resilience in the housing market despite higher effective interest rates.

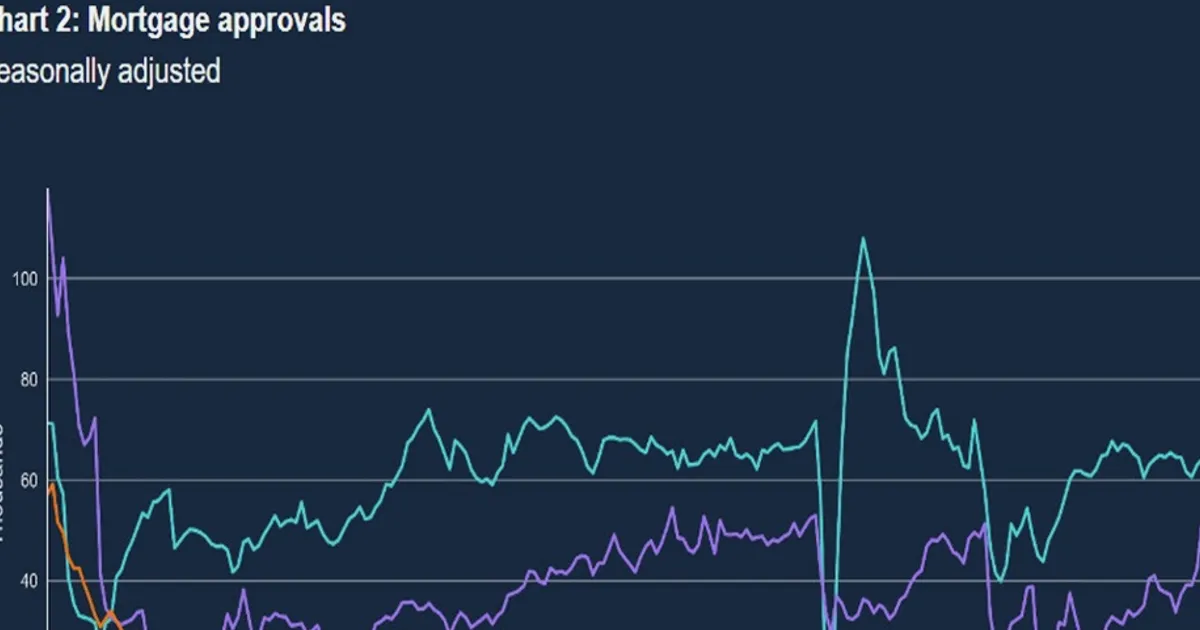

UK mortgage approvals rose to 65,900 in April, up from 64,000 in March and above the six-month average of 63,100, according to the Bank of England's latest money and credit data. The figures indicate continued solid demand for housing loans despite a rise in the effective interest rate on newly drawn mortgages to 4.08%. This increase in approvals comes as the Bank of England maintains its Bank Rate at 5.25%, a level that has been held steady since August 2023. The housing market's resilience is notable given the broader context of elevated borrowing costs and the lagged effects of previous rate hikes, which typically take 12-18 months to fully transmit through the economy.

For interest rate and central bank policy traders, the data point to resilience in the UK housing market, which supports the case for the Bank of England to maintain a cautious stance on rate cuts. Higher mortgage approvals suggest that borrowing activity remains robust, potentially adding to inflationary pressures in the services sector. This is particularly relevant as the BoE's Monetary Policy Committee (MPC) balances its dual mandate of price stability and supporting economic growth. The strength in housing could also influence the yield curve, where short-term rates remain elevated while longer-term yields reflect expectations of future easing. Traders can monitor these trends on NowPrice's live rates dashboard to gauge market expectations for BoE policy, including the pricing of swap spreads and the term premium embedded in gilt yields.

Looking ahead, market participants will focus on upcoming inflation and GDP data to assess the trajectory of UK interest rates. The BoE's next policy decision will be closely watched, with the housing market's strength likely to influence the pace of any future rate adjustments. The effective rate on new mortgages, now at 4.08%, will also be a key indicator of borrowing costs and consumer sentiment. Additionally, traders should monitor the ECB's transmission protection instrument (TPI) for any spillover effects on UK rates, as well as the Fed's balance-sheet runoff and its impact on global term premiums. Any signs of a yield-curve inversion deepening could signal recession risks, while a steepening would suggest confidence in a soft landing.