CLO ETFs Surge as Higher Rates Boost Demand, Private Credit Struggles

Collateralized loan obligation ETFs are attracting record inflows as elevated interest rates boost yields and retail investors seek alternatives to troubled private credit markets.

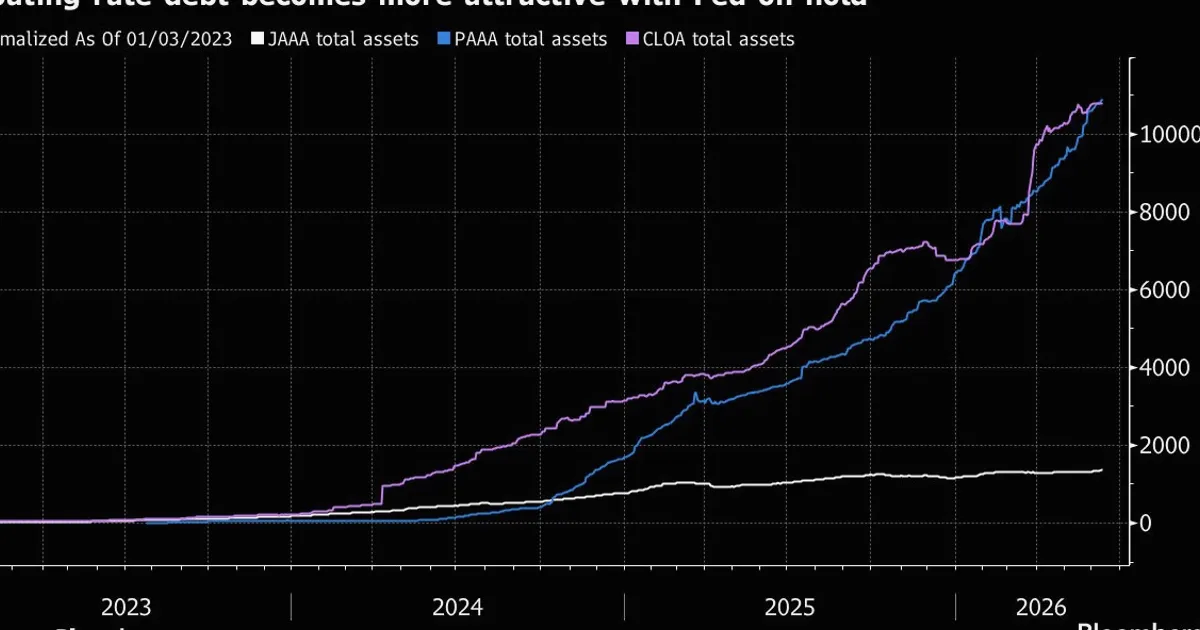

Collateralized loan obligation (CLO) exchange-traded funds are experiencing a surge in demand as higher interest rates boost their yields and retail investors look for safer alternatives to the troubled private credit market. The Fed model, which compares earnings yield to Treasury yield, has historically favored fixed-income products when rates rise, and current CLO ETFs offer yields exceeding 7%, outpacing 10-year Treasuries near 4.5%. This yield advantage has drawn inflows, with CLO ETFs like the Janus Henderson AAA CLO ETF (JAAA) and the Invesco CLO ETF (ICLO) seeing record monthly inflows exceeding $1 billion combined.

Wall Street has responded to this demand by launching new CLO ETFs, which package leveraged loans into diversified portfolios and offer attractive income streams. These products have seen record inflows in recent months, as the Federal Reserve's rate hikes have pushed CLO yields higher. Meanwhile, the private credit sector is facing rising default risks and liquidity concerns, prompting investors to shift toward more regulated and transparent CLO structures. The shift reflects a broader sector rotation out of riskier private debt, which carries higher buyback yields but less transparency, into regulated CLOs that benefit from senior tranche protections and lower options-implied volatility. Live stock prices and charts on NowPrice show how the broader market is reacting to this rotation, with financial sector ETFs also gaining as bank-linked CLO holdings improve.

Looking ahead, traders should monitor the trajectory of interest rates and credit spreads. If the Fed signals a pause or cut, CLO yields may compress, potentially slowing inflows. Additionally, any deterioration in corporate earnings or loan defaults could test the resilience of CLO portfolios. The forward P/E for the S&P 500 currently sits at 20x, suggesting elevated equity valuations that could amplify rotation if earnings disappoint. Breadth indicators, such as the percentage of stocks above their 50-day moving average, remain weak, hinting at selective risk appetite. The upcoming earnings season will provide clues on whether the private credit stress will spread to the broader leveraged loan market, with key reports from major banks and private lenders due in the coming weeks.