Mortgage Hedging ‘Beast’ Returns to Treasury Market, Adding Volatility

The return of mortgage hedging flows is expected to amplify Treasury volatility as investors adjust to shifting rate expectations and prepayment risks.

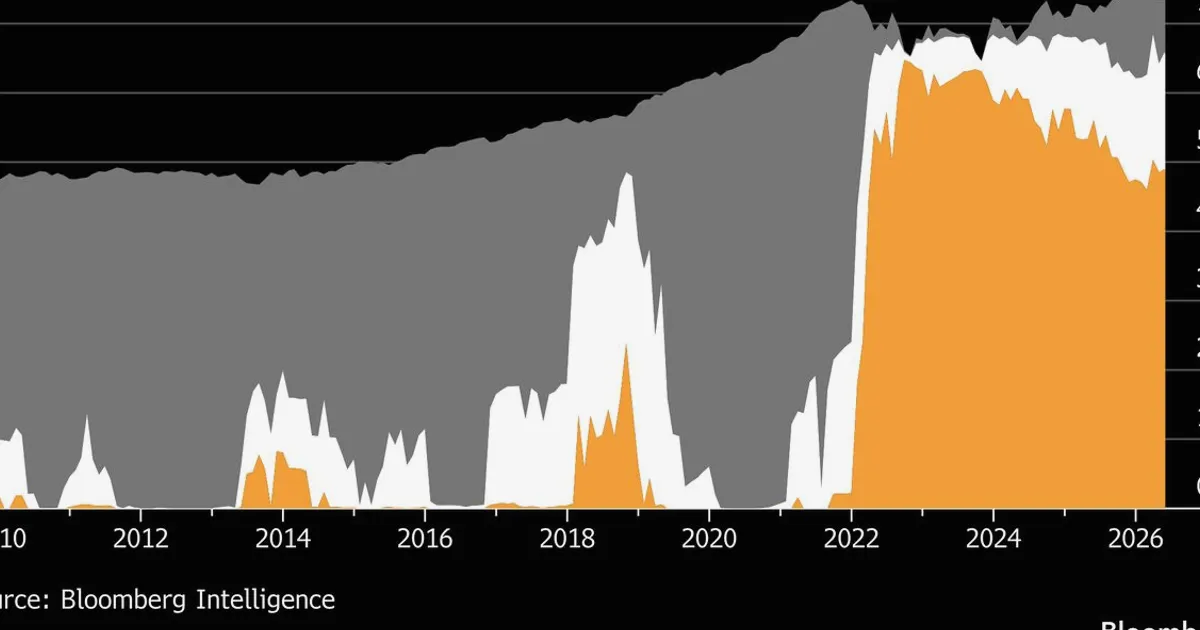

A resurgence of mortgage hedging activity is injecting fresh volatility into the US Treasury market, reviving a dynamic that traders call the 'mortgage beast.' At the height of last month's bond selloff, portfolio managers like Vishal Khanduja at Vanguard detected early signs of this trend, which now appears to be accelerating as interest rate uncertainty persists.

Mortgage servicers and investors use Treasury futures and swaps to hedge against prepayment risk and duration shifts. When rates rise sharply, prepayments slow, extending the duration of mortgage-backed securities (MBS), forcing hedgers to sell Treasuries to rebalance. Conversely, when rates fall, prepayments accelerate, shortening MBS duration and prompting Treasury buying. This feedback loop can amplify bond market moves, adding to the volatility that equity traders must monitor as a key driver of risk sentiment and discount rates for stocks. For the latest Treasury yields and stock index levels, check NowPrice's real-time quotes.

Traders should watch for upcoming economic data that could shift rate expectations, such as employment reports and inflation readings. The magnitude of mortgage hedging flows will depend on how far and fast yields move from current levels. A sustained break above key yield thresholds could trigger a more aggressive hedging cycle, while a stabilization might keep the 'beast' at bay. Market participants will also monitor MBS convexity metrics and dealer positioning for clues on the scale of these flows.